Jun 30, 2026

The Pros and Cons of Owning Vacation Homes

If you have recently come into sudden wealth through an inheritance, business sale, or legal settlement, the pros and cons of owning vacation homes deserve a clear answer before you buy: the upside can include personal enjoyment, family memories, rental income potential, long-term appreciation, and more flexibility in how you live, while the downside often includes ongoing and unexpected costs, time commitment, vacancy risk, market swings, and the emotional limits of being tied to one place. The idea of owning a beach house on the Gulf Coast or a mountain cabin in North Carolina sounds like the reward you have earned, but a vacation home is both a lifestyle choice and a major financial decision that can affect your retirement, taxes, long-term wealth, and family legacy.

It should generally be treated as a lifestyle purchase first and an investment second. Owning a vacation home can be rewarding when the numbers and the life plan line up, but it can also complicate cash flow, stewardship, and future planning when they do not. This article walks through the key pros and cons of owning vacation homes, the lifestyle questions to ask, the financial and tax implications to weigh, the market and location factors to review, and the alternatives to ownership you may want to consider. At Third Act Retirement Planning, a fee-only financial advisory firm based in Marietta, Georgia, we help people with sudden wealth decide whether a second home fits their retirement and legacy plan and how a fiduciary advisor can support that decision. Our goal is not to sell you a house. It is to help you think clearly and biblically about stewardship, lifestyle, and the housing market before you commit.

Pros of Owning a Vacation Home

When chosen wisely, a vacation home can deliver emotional, relational, and financial benefits that genuinely improve your life. Here are the advantages worth considering.

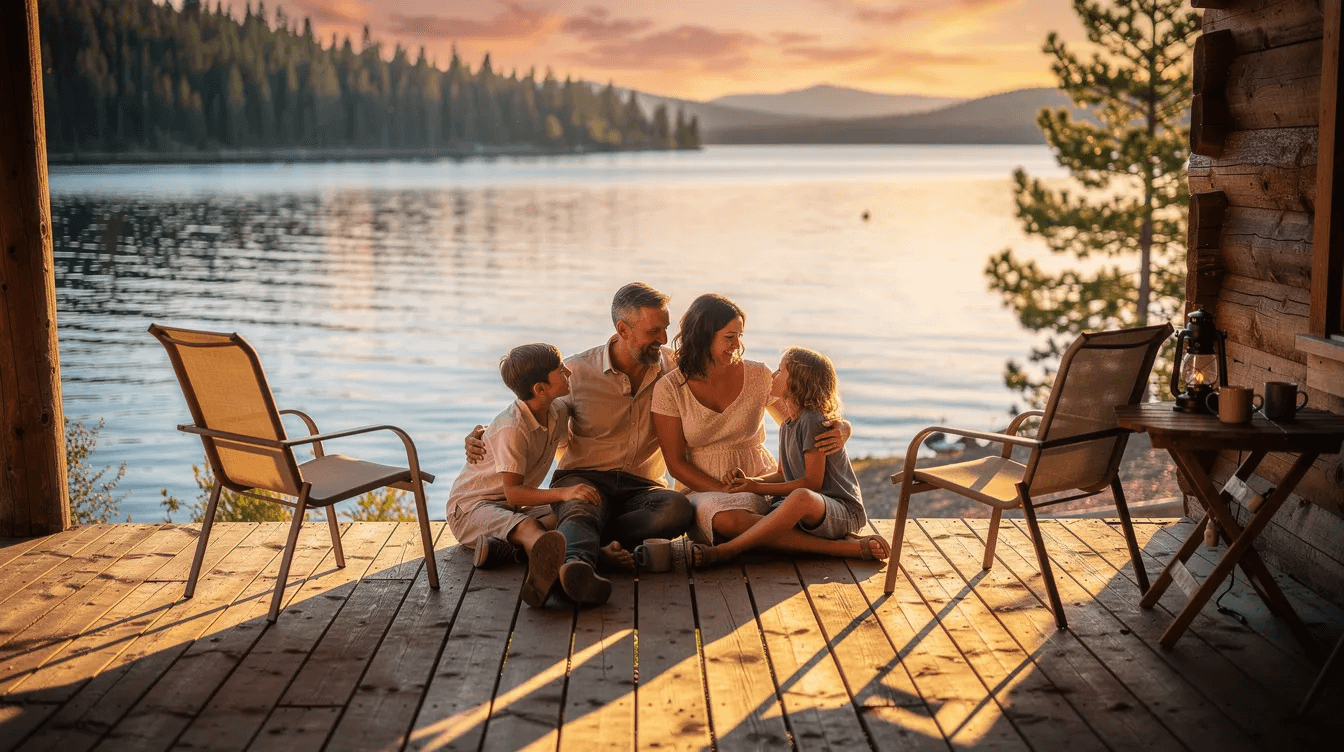

Personal enjoyment and family memories. Owning a vacation home can provide emotional benefits and create lasting memories. Having a dedicated place for holidays, summers, and long weekends means your kids and grandkids know exactly where they will gather year after year. Owning a vacation home can create priceless family memories that no hotel stay can replicate.

Relationship building. A vacation house becomes a hub for extended family, church friends, and reunions. Think Thanksgiving at a mountain cabin or summer weeks at a lake house where cousins grow up together. Community integration can build friendships in a new area, turning a property into a second community rather than just a getaway. Many buyers eventually convert a vacation home into a retirement residence, making those relationships even more valuable over time.

Rental income potential. Turning a second home into a vacation rental on platforms like Airbnb or Vrbo can help offset your mortgage, taxes, and HOA dues. Rental income can offset mortgage payments, taxes, and maintenance costs, especially in popular destinations that often offer better rental opportunities. Dynamic pricing optimizes rental rates based on market conditions, and listings using dynamic pricing saw occupancy around 57% compared to 44% for static-rate properties. That extra income makes a real difference. You can also write off business-related expenses for your vacation home when it qualifies as a rental property under IRS rules.

Long-term appreciation. Vacation homes can appreciate in value over time. Highly desirable vacation locations can appreciate and act as an inflation hedge. Florida, for example, saw roughly 71.2% home value gains over five years ending early 2026, though past performance is never guaranteed.

Lifestyle flexibility and tax benefits. A beach condo lets you escape winter. A mountain property puts you near grown children for part of the year. With proper structuring, you may deduct mortgage interest, property taxes, and certain rental expenses. However, these benefits require careful coordination with a CPA.

For some clients at Third Act Retirement Planning, a vacation home is part of a purposeful retirement strategy, not just a luxury purchase.

Cons of Owning a Vacation Home

Owning a vacation home is rarely passive. It is often more expensive and more stressful than people expect. Here is what to watch for.

Ongoing costs add up fast. Vacation homes often require significant financial responsibility. Costs include two mortgages, higher insurance premiums, and property taxes. A homeowner must pay property taxes on a vacation home without primary residence exemptions, and utilities run year-round even when the house sits empty. Insurance costs may increase for vacation homes in risky areas, especially coastal properties exposed to hurricanes and flooding. Higher insurance costs may apply for vacation homes in risky areas like the Florida Panhandle, where salt air and storm exposure accelerate wear on roofs, HVAC systems, and exterior finishes.

Unexpected expenses. Unexpected repairs can significantly impact vacation home budgets. A single roof failure, storm damage event, or special HOA assessment can cost tens of thousands of dollars in a year you did not plan for. Owning a vacation home incurs ongoing maintenance costs that compound when you defer them.

Time commitment and stress. Second homes can generate stress from maintenance and management. Trying to maintain a home from a distance is challenging. Coordinating contractors, cleaners, and repairs from hundreds of miles away while managing paying guests, bookings, and reviews is a real hassle. Owning a vacation home requires significant financial and logistical management. Maintenance responsibilities can add costs or require hiring local managers.

Vacancy reality. Many vacation homes sit empty for 10 to 11 months yearly. Average occupancy for vacation rentals slipped to roughly 51% in 2025, meaning a majority of days carry full cost with zero income. Double expenses include two mortgages and higher property taxes, whether or not anyone is staying in the property.

Market and concentration risk. Vacation markets are more volatile than primary residence markets and can be harder to sell in a downturn. Tying a large portion of your net worth to one asset in one location exposes you to local economic, environmental, or regulatory shocks. Owning a second home typically requires larger down payments, often 20% or more, with mortgage rates roughly 0.25% to 0.50% higher than for your primary residence.

Emotional risk. Owning a vacation home locks you into vacationing in a single location. Owning a vacation home can limit travel to other locations, and after 10 to 20 years, your travel preferences, family dynamics, or health may change in ways you did not anticipate.

Lifestyle Questions to Ask Before Buying a Vacation Home

Lifestyle fit often matters more than spreadsheets when it comes to owning a vacation home. Before you spend money on a purchase, ask yourself these questions:

How much time will you realistically spend there? If you will not visit at least 6 to 8 weeks per year within three years of purchase, think carefully. Many owners are surprised how few weeks they actually use the property.

Do you enjoy returning to the same place? If you and your family value exploring new destinations and other travel over returning to one spot, ownership may feel restrictive rather than glad.

Will you join the local community? Consider whether you want to create roots near the vacation house, joining local churches, clubs, or volunteer services. A property that feels like home in advance of retirement is different from one that just collects dust on the calendar.

Have you tried before you buy? Rent in the same town or on the same street for at least one full season. You will discover daily realities like weather, traffic, crowds, and off-season quiet that brochures never mention. Vacation rental management includes regular maintenance and guest services, and experiencing that firsthand helps you decide if the owner lifestyle fits. Marketing requires eye-catching photos and compelling descriptions, but living there day to day is a different story.

Does it align with your calling? Reflect on whether this purchase fits your family priorities and the kind of memories you want to create. Owning a vacation home may increase your property tax obligations and shift your spending money choices for decades.

Financial Planning: Is a Vacation Home a Smart Investment Property for You?

Buying a vacation home should be evaluated as part of a complete financial and retirement plan, not in isolation.

Cash flow analysis. Project all annual costs: mortgage, taxes, insurance, utilities, maintenance, management, and travel to the property. Compare those against expected rental income and your personal budget. For a $600,000 vacation home with 20% down, monthly carrying costs including taxes, insurance, and maintenance can easily reach $4,650 or more.

Investment property vs. personal retreat. A true investment property is managed for maximum occupancy and return. A personal second home is managed around your family's calendar. Mixing the two goals often leads to disappointment on both fronts. Renting out your vacation home incurs federal taxes on income, and renting out a vacation home requires compliance with local laws. Consult a tax professional to maximize your vacation home tax deductions, handle rental income reporting, and understand tax strategies for your situation.

Opportunity cost. Using $400,000 cash for a vacation house instead of investing in a diversified portfolio could significantly change your retirement readiness over 20 to 30 years.

Retirement impact. A vacation home affects withdrawal rates, Social Security timing, savings, and your ability to fund healthcare and long-term care later in life. Third Act Retirement Planning helps clients model different scenarios-own, rent, or invest-to see the long-term implications on their financial plan and estate.

Location, Regulations, and the Current Housing Market

Location is the most important factor for vacation home buyers, and it matters even more for vacation rentals and second homes than for primary residences.

Proximity matters. Research shows 64% of buyers prefer a second home within four hours of commute, and 87% of buyers want to drive to their vacation home rather than fly. For families near Atlanta or Charlotte, that puts two regions in play: the Blue Ridge mountains and the Southeast coast. Most buyers prefer homes on water or with mountain views, which tends to support demand and value.

Climate and risk. Beach properties face hurricanes, flooding, and rising insurance costs in states like Florida. Mountain and lake homes carry wildfire risks and winter access issues. Weigh these carefully when evaluating a location.

Local regulations. Local laws for vacation rentals vary significantly by location. Some cities and HOAs have strict limits or outright bans on short term rentals, and local zoning laws can restrict rental income generation. Hiring a property management company can reduce owner responsibilities, but it does not eliminate regulatory risk.

The housing market in 2026. Home prices remain elevated after the pandemic surge, and second-home mortgage rates sit in the low- to mid-7% range. Second-home mortgage volume dropped to about 86,600 in 2024, down from over 250,000 in 2021. Demand for vacation homes is cooling. Work with a local real estate agent experienced in vacation homes and coordinate with a fiduciary financial advisor before committing.

Alternatives to Owning a Vacation Home

Many of the benefits of a vacation home can be achieved without full ownership.

Rent instead of buy. Renting vacation homes through vacation rentals platforms several times a year preserves flexibility and capital. You can visit different destinations, stay in a hotel when it suits you, and avoid the hassle of long-distance property management.

Timeshares and fractional ownership. These exist but come with complexity, fees, and resale challenges. Proceed with thorough due diligence and healthy skepticism.

Set-aside travel budgets. Build a generous travel fund into your sustainable spending plan. You can create incredible family memories without tying money up in a single property.

Redirect the capital. For some Third Act Retirement Planning clients, redirecting vacation-home dollars into diversified investments, charitable giving, or family experiences can better support their calling and legacy goals.

Compare these alternatives side by side with purchasing a second home over a 10 to 20 year timeframe before you decide.

How Third Act Retirement Planning Can Help You Decide

At Third Act Retirement Planning, we work with clients who are considering buying a vacation home after an inheritance, business sale, NIL deal, or other windfall. If you have recently received a large sum of money, a vacation home may be on your mind, and we want to help you think through it clearly.

As a fee-only fiduciary firm, we do not earn commissions on real estate or mortgages. Our advice is focused entirely on what is best for your retirement, tax, and legacy plan. We integrate biblical wisdom and stewardship into every conversation, viewing a second home or vacation rental not only as an asset but as a tool to serve family, church, and community.

Our process is straightforward: a discovery call, gathering your financial details, scenario modeling (own vs. rent vs. invest), tax and estate planning review, and an ongoing plan for monitoring the vacation home decision over time. If you are near Marietta, Georgia or anywhere across the U.S. and weighing whether buying a vacation home in the next 12 to 24 months fits your life, we would be glad to talk.

Conclusion: Weighing the Pros and Cons of Owning a Vacation Home

Owning a vacation home can be wonderful for family memories and potential wealth building, but it also comes with significant costs, risks, and responsibilities that demand honest evaluation. The key tension is real: lifestyle joy and potential rental income on one side, ongoing expenses, time demands, and housing market uncertainty on the other.

Take time to pray, discuss it with your family, and run the numbers with a trusted financial advisor before selling yourself on a dream that may not fit your plan. News of a lucky deal or a press release about a hot vacation market in Canada or anywhere else should never rush a decision this large.

If you are ready to explore whether a second home belongs in your retirement and legacy strategy, reach out to Third Act Retirement Planning. We will help you model the scenarios, weigh the stuff that matters, and build a plan rooted in purpose rather than impulse.