Oct 23, 2025

Mastering the Rules of Inheritance Tax: Essential Insights and Tips

Inheritance tax is a levy on the assets beneficiaries receive from a deceased individual’s estate. Understanding the rules of inheritance tax is crucial for effective estate planning and to avoid unexpected tax burdens. This article will guide you through the fundamental guidelines, distinctions between inheritance and estate tax, state-specific rules, calculation methods, exemptions, and strategies to minimize your tax liability.

Key Takeaways

Inheritance tax is imposed on beneficiaries receiving assets from a deceased person’s estate, whereas estate tax is charged on the total value of the estate before distribution.

States imposing inheritance taxes have varying rates and exemptions that can significantly impact the net value inherited, requiring careful consideration for estate planning.

Consulting a tax professional is crucial for navigating the complexities of inheritance tax laws and implementing strategies to minimize tax liabilities.

Understanding Inheritance Tax

Inheritance tax is a levy imposed on heirs. They pay this tax on the assets inherited from a deceased individual’s estate. These assets, collectively known as an inheritance, can include anything of value passed down after someone’s estate, such as real estate, investments, and personal property. Here, "someone's estate" refers to the total assets and possessions left by the deceased. Inheritance tax is levied on these assets and imposes inheritance taxes.

Distinguishing inheritance tax from estate tax is key. Inheritance tax is paid by the individuals receiving the assets, while estate tax is levied on the total value of the deceased person’s estate before distribution. The deceased person's estate is the collection of all assets and possessions managed and distributed after death, often involving legal responsibilities such as estate taxes and executors handling the distribution according to the will. The estate tax, often called the “death tax,” reduces the overall amount available to heirs since it is paid by the estate. Conversely, inheritance tax impacts beneficiaries based on the assets they receive. This distinction determines who bears the tax burden—whether it’s the estate or the individual beneficiaries. Due to high exemption thresholds, only a small percentage of estates are subject to federal estate taxes.

Inheritance taxes can vary significantly depending on state laws, meaning the tax implications for heirs can differ widely depending on where the deceased person lived. Grasping these differences aids in effective estate planning, ensuring heirs are not surprised by unexpected tax bills. How inheritance tax works depends on several factors, including state laws, the relationship to the deceased, and exemption thresholds.

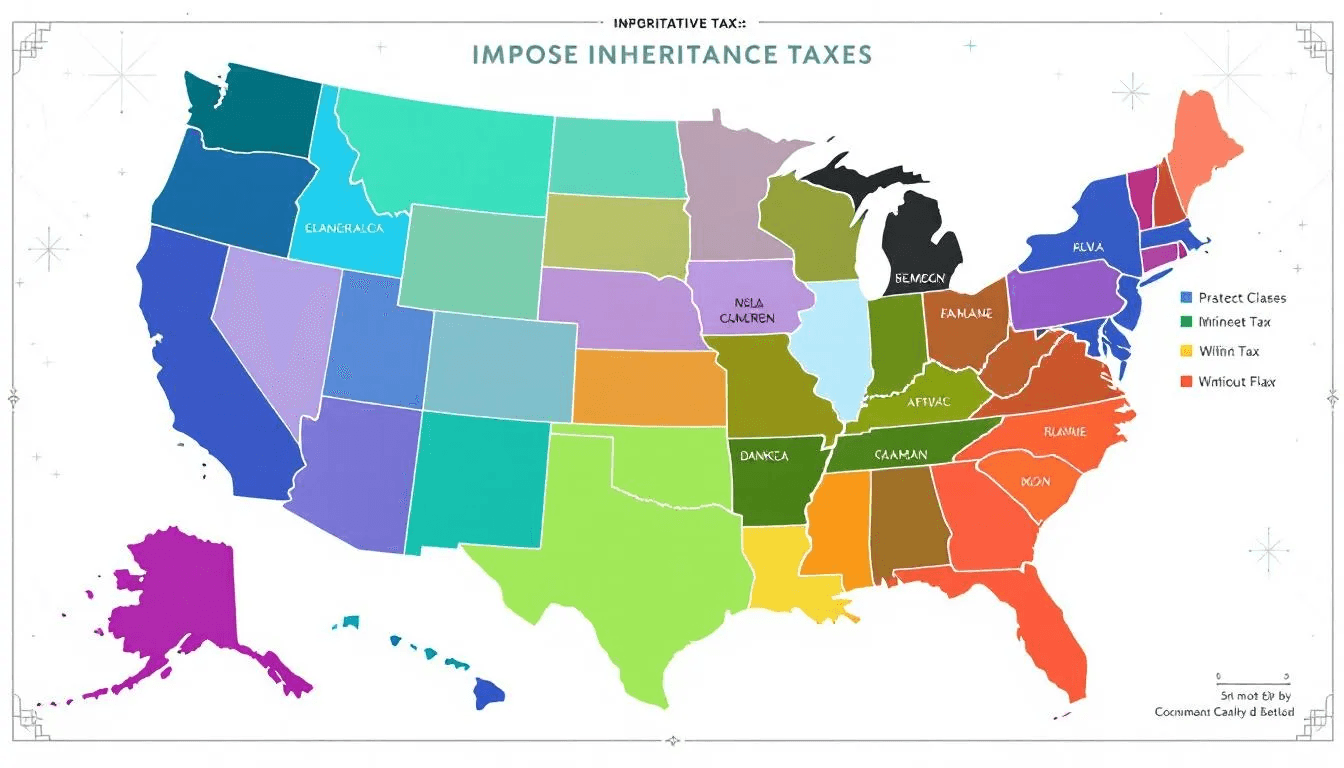

States That Impose Inheritance Taxes

Inheritance taxes are not imposed by most states. However, six states that do impose such taxes are Kentucky, Maryland, Nebraska, New Jersey, Pennsylvania, and Iowa (with Iowa, Kentucky, Maryland, and Nebraska being notable examples). Each of these states has its own specific rates and exemptions, which can impact the net value passed on to heirs. For instance, Kentucky has inheritance tax rates ranging from 4% to 16% (as outlined by the Kentucky Department of Revenue), while New Jersey’s rates range from 11% to 16%.

Maryland charges a flat inheritance tax rate of 10%, and Nebraska’s rates range from 1% to 15%. In New Jersey, certain family members, such as surviving spouses, civil union partners, domestic partners, parents, grandparents, children, stepchildren, grandchildren, and great-grandchildren, are exempt from inheritance tax. Similarly, Pennsylvania offers exemptions to surviving spouses and children under 21.

Iowa plans to eliminate its inheritance tax by January 1, 2025. Knowing these state-specific rules is vital for estate planning or receiving an inheritance, as they significantly affect the tax burden and overall inheritance. The Iowa Department emphasizes the importance of understanding these regulations. While Rhode Island does not impose an inheritance tax, it does have its own estate tax regulations, which are important to consider for estate planning.

Federal vs. State Inheritance Taxes

A key distinction in understanding inheritance tax lies in the differences between federal government and state taxes. The United States does not impose a federal inheritance tax. This means that inheritance received by beneficiaries is not taxed at the national level. Instead, what exists at the federal level is the federal estate tax, which is levied on the total value of an estate before it is distributed to the beneficiaries. Additionally, it is important to note that federal tax obligations may arise in other contexts.

The federal estate tax and state inheritance taxes differ in the following ways:

The federal estate tax impacts the estate itself rather than the individuals receiving the assets.

The tax burden of the federal estate tax is borne by the estate, potentially reducing the overall amount available to heirs.

State inheritance taxes are paid by the beneficiaries, meaning the beneficiary pays the state inheritance tax on the value of the assets they receive.

The rates of state inheritance taxes can vary significantly depending on the state and the relationship of the heir to the deceased, including considerations of federal taxes.

These distinctions are vital for effective estate planning. While the federal estate tax impacts the total estate value, a key difference is that state inheritance taxes can add an additional burden on the beneficiaries, making it crucial to consider both types of taxes in your planning.

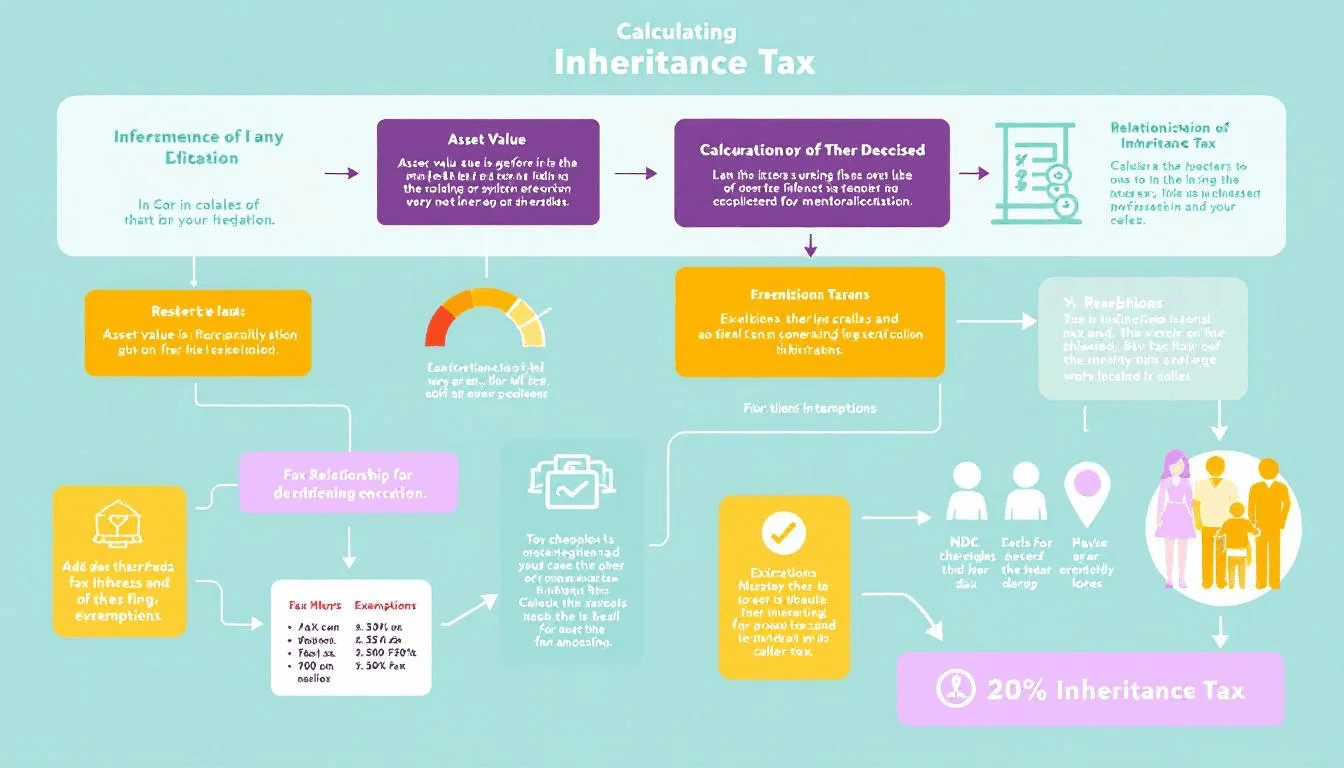

How Inheritance Tax is Calculated

The calculation of inheritance tax hinges on several factors, including the value of the inherited assets and the recipient’s relationship to the deceased. The inheritance tax rate often depends on the recipient's relationship, with closer relatives such as spouses and children typically receiving more favorable tax treatment compared to distant relatives or non-relatives. State legislation plays a significant role, as different states have varied methods and rates for calculating inheritance tax.

Inheritance tax rates can be either flat or graduated. Flat rates apply uniformly regardless of the inheritance size, while graduated rates increase with the value of the inheritance. Additionally, exemption thresholds vary by state, meaning that inheritance tax is only applied to amounts exceeding a certain amount. Taxes are only due if the inheritance surpasses certain thresholds, which can significantly impact the tax owed by beneficiaries.

Accurately valuing the decedent’s estate at fair market value is crucial for calculating the inheritance tax. This process involves accounting for all assets, such as real estate, investments, and liabilities, at the time of the decedent’s passing. The calculation is only necessary if the estate exceeds certain thresholds. Using an alternate valuation date can lower the gross estate value, thus reducing estate tax liability. These factors can help beneficiaries and estate planners manage and potentially lessen the inheritance tax owed.

Exemptions and Thresholds for Inheritance Tax

Exemptions and thresholds for inheritance tax vary widely among the states that impose such taxes. For example, in New Jersey, the certain threshold for inheritance tax as of 2024 is $25,000. Maryland offers a $1,000 exemption for recipients other than the spouse or close family members. These exemptions can significantly affect the inheritance tax calculations and the net value passed on to heirs.

Spouses are generally exempt from paying inheritance tax on property inherited from their deceased spouse. In Iowa, many beneficiaries, including the surviving spouse, certain descendants, and other beneficiaries, are exempt. These exemptions help reduce the tax burden on family members and ensure more of the estate’s value remains within the family.

Additionally, exemptions for other relatives can vary based on the relationship to the deceased individual. For instance, in Kentucky, exemptions for other relatives may be up to $1,000 depending on the relationship. In Nebraska, the exemption ranges for close relatives vary from $40,000 to $100,000 depending on the relationship. Understanding these exemptions is essential for effective estate planning and minimizing tax liability.

It is important to note that other rules may apply, such as special discounts, exceptions, or specific conditions that can affect inheritance tax calculations.

Paying Inheritance Tax: Process and Deadlines

Paying inheritance tax involves specific processes and deadlines that beneficiaries must adhere to:

Beneficiaries are generally responsible for filing inheritance tax returns and may need to pay taxes on inherited assets.

In some states, executors may file the returns and pay taxes instead.

These returns and tax payments are typically due within several months of the decedent’s death.

It is important to act promptly to meet these deadlines, as the timing for paying taxes is directly linked to the decedent's death.

In Pennsylvania, beneficiaries can receive a 5% discount for paying inheritance tax within three months of the decedent’s death, according to the Pennsylvania department. In Kentucky, a 5% discount is available. This applies when inheritance taxes are paid within nine months of death. These incentives underscore the importance of timely payment to avoid additional financial burdens.

While specific penalties for late payment were not provided, it is common for late payments to incur interest or fines. Therefore, staying informed about deadlines and ensuring timely payment is crucial to avoid additional costs and complications.

Inheritance Tax Returns and Compliance

Filing inheritance tax returns demands strategic precision—a reality I've witnessed countless times when beneficiaries and executors fumble through inherited assets in states like Kentucky, Maryland, Nebraska, New Jersey, and Pennsylvania, where inheritance tax strikes decisively. The responsibility lands squarely on beneficiaries or estate executors, depending on specific state regulations. Mastering this process isn't optional—it's essential to eliminate unnecessary tax burdens and achieve complete regulatory compliance.

The strategic approach begins with calculating inheritance tax liability based on inherited property values and the beneficiary's relationship to the deceased. Each state wielding inheritance taxes operates with distinct rates that vary dramatically. Take New Jersey and Pennsylvania—inheritance tax rates span from 4.5% to 16%, depending entirely on the recipient's relationship to the decedent and total asset values received. Accurately determining fair market value of inherited assets becomes absolutely critical for calculating correct tax rates and total obligations.

Inheritance tax returns operate under rigid deadlines—typically several months post-death. Missing these deadlines triggers penalties and interest charges, unnecessarily inflating your tax burden. States like Kentucky and Pennsylvania offer early payment discounts, rewarding prompt compliance with immediate savings opportunities.

Consulting a seasoned tax professional proves non-negotiable for optimal outcomes. A qualified expert delivers precise inheritance tax return preparation, identifies every available exemption and deduction, and ensures correct tax rate application. This becomes absolutely essential when managing complex estates or when the deceased owned multi-state properties—complexity demands expertise.

Beyond inheritance tax, beneficiaries must strategically address capital gains tax obligations. When inherited assets like stocks or real estate appreciate and sell later, capital gains tax strikes the profit margin. Your tax liability depends on the asset's stepped-up basis at inheritance and your current taxable income level.

Minimizing overall tax liability requires proactive estate planning strategies—utilizing lifetime gift tax exemptions or establishing irrevocable trusts. These approaches systematically reduce taxable estate size and potentially eliminate inheritance tax on specific assets entirely.

Ultimately, maintaining compliance with inheritance tax laws and filing accurate, timely returns isn't just important—it's fundamental for beneficiaries and executors seeking maximum wealth preservation. Working with knowledgeable tax professionals and understanding specific requirements in Maryland, Nebraska, New Jersey, and beyond enables you to decisively manage tax obligations, minimize burdens, and secure maximum benefit from inherited assets.

Strategies to Minimize Inheritance Tax Liability

Minimizing inheritance tax liability is a key concern for many beneficiaries and estate planners. One effective strategy to avoid inheritance tax is to establish irrevocable trusts, which allows assets to be transferred to heirs without undergoing the probate process. Trusts can provide significant tax advantages and help preserve wealth for future generations. These and other estate planning strategies are commonly used to avoid taxes on inherited assets.

Another strategy is to make annual gifts up to a specified limit, which do not impact the lifetime estate tax exemption. Additionally, donating a portion of the inheritance to charity can help avoid taxable gains and provide tax deductions. These actions can significantly reduce the taxable estate and the overall tax burden.

Consulting a tax professional is crucial for effectively crafting these strategies. Financial professionals can:

Manage complex financial matters

Identify potential tax issues in estate planning Accountants can also help:

Implement strategies to minimize or avoid inheritance taxes

Ensure more of the estate’s value is retained by the heirs.

Capital Gains Tax on Inherited Assets

Capital gains tax on inherited assets is another important consideration. The “stepped-up basis” rule allows inherited assets to be valued at their market price at the time of the owner’s death, which can significantly reduce potential capital gains tax when the asset is sold. This means that the original purchase price is replaced with the asset’s value at the time of inheritance, minimizing taxes upon sale.

Capital gains tax is only triggered when the inherited asset is sold for more than its stepped-up basis. This provision allows heirs to potentially sell the inherited property without incurring a significant tax burden if the asset’s value has not appreciated much since the time of inheritance, and they may need to pay capital gains tax if it has.

However, if the asset appreciates in value after inheritance, capital gains tax will apply to the increased value. Knowing how capital gains tax applies to inherited assets is crucial for effective estate planning and helps heirs manage their tax obligations efficiently.

Common Misconceptions About Inheritance Tax

There are several common misconceptions about inheritance tax that can lead to confusion and unexpected tax liabilities. One misconception is that gifting a property can fully avoid tax liabilities; however, if the giver dies within seven years, the property’s value may still count towards their estate. This highlights the importance of understanding the rules surrounding lifetime gifts and inheritance tax.

Another misconception is that inheritance tax applies solely to real estate. In reality, virtually all assets in an estate may be subject to this tax, including investments, personal property, and other assets. However, not all inheritances are inheritance taxable; whether an inheritance is taxable depends on state laws and the value of the estate. This broad application means that beneficiaries must be aware of the full scope of inheritance tax to avoid surprises.

Understanding these common myths is crucial for navigating inheritance tax obligations effectively. By dispelling these misconceptions, beneficiaries and estate planners can make more informed decisions and better manage their tax liabilities.

Consulting a Tax Professional

Consulting a tax professional is essential to navigate the complex landscape of inheritance tax laws effectively. Estate planning attorneys, CPAs, and financial planners can provide valuable insights and help manage inheritance tax obligations. Their expertise is particularly important for individuals with high net worth or specific tax obligations.

Inheritance tax laws can vary significantly based on different factors, making professional guidance crucial. A tax professional can help beneficiaries and estate planners understand the applicable tax laws, identify potential tax issues, and implement strategies to minimize tax liability.

Working with a tax professional ensures that you are well-prepared to handle inheritance tax obligations, preserving more of the estate’s value for future generations. Their expertise can provide peace of mind and help you navigate the complexities of estate and inheritance taxes effectively.

Summary

In summary, understanding inheritance tax is crucial for effective estate planning and minimizing tax liabilities. This guide has covered the basics of inheritance tax, the states that impose these taxes, the differences between federal and state taxes, calculation methods, exemptions, and strategies to minimize tax burdens.

By staying informed and consulting with tax professionals, you can navigate the complexities of inheritance tax laws and ensure that your estate planning preserves as much wealth as possible for future generations. Armed with this knowledge, you are better equipped to make informed decisions and manage your inheritance tax obligations effectively.

Frequently Asked Questions

What is the difference between inheritance tax and estate tax?

The key difference between inheritance tax and estate tax is that inheritance tax is assessed on individuals who receive assets, whereas estate tax is imposed on the overall value of the deceased’s estate—known as the decedent's estate—which includes all assets and possessions at the time of death, prior to distribution. Understanding these distinctions is crucial for effective estate planning.

Which states impose inheritance taxes?

Six states impose inheritance taxes: Kentucky, Maryland, Nebraska, New Jersey, Pennsylvania, and Iowa. It is important to be aware of these taxes when planning estate matters. The familial relationship between the beneficiary and the deceased can affect exemption status and tax rates, with closer relatives often receiving greater exemptions. In some states, a domestic partner may also be recognized for exemption purposes, similar to spouses and other close relatives.

Are there federal inheritance taxes in the United States?

There is no federal inheritance tax in the United States; however, there is a federal estate tax that applies to the entire value of an estate before it is distributed to beneficiaries.

How can I minimize my inheritance tax liability?

To minimize your inheritance tax liability, consider establishing trusts, making annual gifts, and donating to charity, while also seeking advice from tax professionals for tailored strategies. These approaches can effectively reduce the taxable portion of your estate.

What is the stepped-up basis for inherited assets?

The stepped-up basis enables inherited assets to be assessed at their market value at the time of the owner's death, which helps minimize capital gains tax upon sale. This can significantly benefit heirs when selling the inherited assets.