Nov 20, 2025

Buffer Annuities: A Smart Way to Limit Your Investment Risk

Buffer annuities let you reduce investment risk while still benefiting from market growth. As a relatively new solution, buffer annuities offer investors a way to manage risk and capture market gains with innovative features. They protect your principal by absorbing some market losses. This article covers how buffer annuities work, their key features, and their benefits and downsides.

Key Takeaways

Buffer annuities offer a blend of growth potential and downside protection, making them suitable for risk-averse investors.

These annuities absorb a specified percentage of market losses, usually between 10% and 30%, while linking growth to market index performance.

Buffer annuities can provide guaranteed income options, subject to the claims-paying ability of the issuing insurance company.

Investors should evaluate their risk tolerance, understand market conditions, and consult financial advisors to make informed decisions regarding buffer annuities.

Understanding Buffer Annuities

A buffer annuity is an annuity product that strikes a balance between growth potential and protection against market downturns. These tax-deferred investments allow you to participate in market growth while limiting your exposure to downside risk. They provide a unique combination of market-linked growth and principal protection, making them an attractive option for investors wary of volatility.

The primary appeal of buffer annuities is their capacity to reduce risk during market downturns while still offering potential investment gains. However, there is a cap on the growth potential, and some risk of loss remains. Nonetheless, buffer annuities are designed to offer a balanced approach, protecting against significant losses while providing opportunities for growth.

Buffer annuities are a type of annuity contract that can be customized with features such as buffers and floors to meet different retirement income needs.

Understanding the definition and mechanics of buffer annuities provides a clearer appreciation of their benefits. The features and guarantees of buffer annuities depend on the financial strength of the insurance carrier and the issuing company.

Definition of Buffer Annuities

Buffer annuities are designed to offer protection against market downturns while allowing for growth linked to market performance. These annuities absorb the first 10% of market losses, providing a buffer that mitigates risk for investors during downturns.

The credited returns in buffer annuities are determined by the index's performance, but are subject to cap and participation rates that may limit the actual amount credited to the contract.

In essence, buffer annuities combine protective features with growth potential, creating a unique investment option with built-in loss protection.

How Buffer Annuities Work

The mechanics of buffer annuities revolve around linking investment growth to the performance of a market index over a specified term, usually ranging from one to six years. This setup allows investors to benefit from market gains while offering a level of downside protection. Buffer annuities may offer a range of investment options tied to different market indexes or strategies, allowing investors to select options that align with their financial objectives and risk tolerance. When the market index performs well, the value of the annuity increases; when the market declines, the buffer mechanism kicks in to absorb a portion of the losses.

Linking investment growth to a market index, buffer annuities offer a blend of potential upside and risk mitigation, appealing to those looking to benefit from market movements without full exposure to market risks.

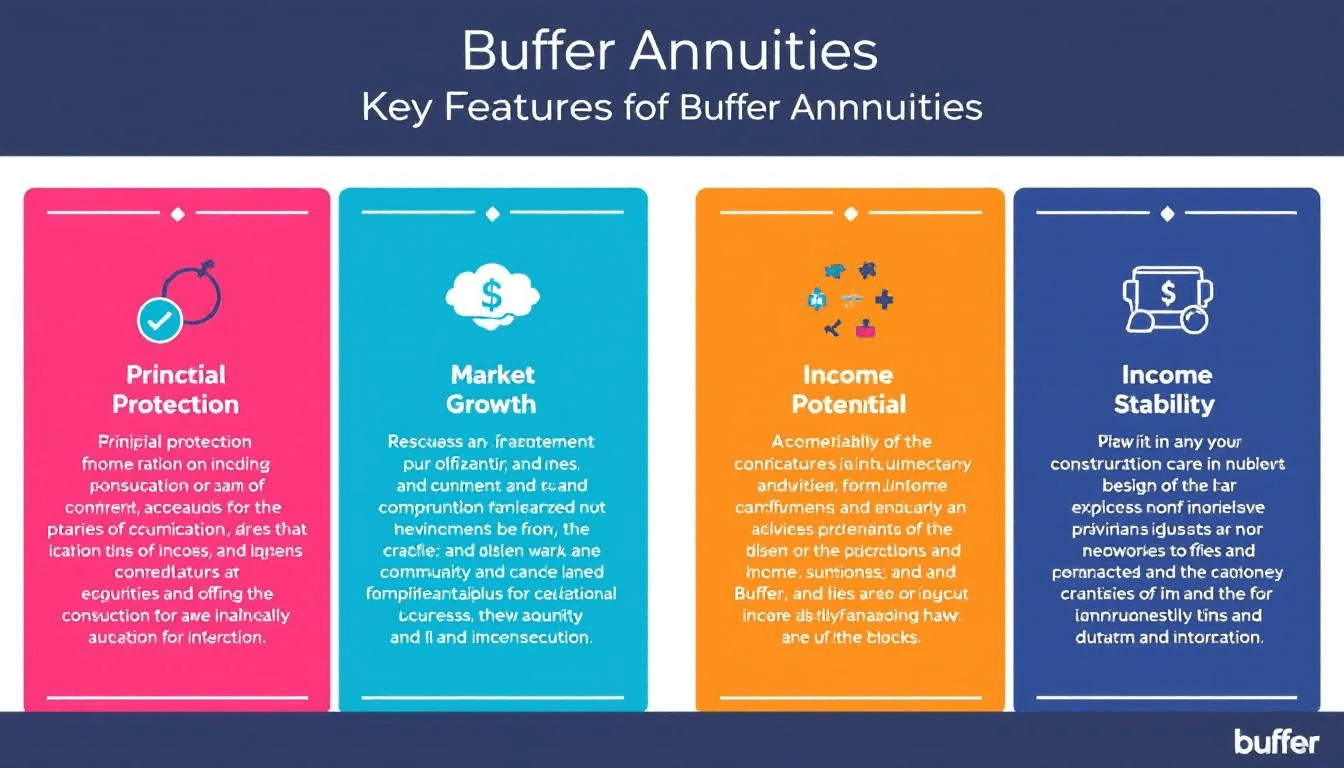

Key Features of Buffer Annuities

Buffer annuities protect against losses while still allowing for potential growth, blending market growth opportunities with a safeguard against significant losses.

These unique features make them a valuable investment tool for balancing risk and reward.

The Buffer Mechanism

A standout feature of buffer annuities, the buffer mechanism absorbs losses typically ranging from 10% to 30% depending on the product, with common buffer levels including 10%, 20%, and up to 30% of market losses.

For example, if the market index experiences a 10% loss, the insurance company absorbs this loss, keeping the return flat. However, if the market drops by 25%, the insurer absorbs the first 10%, resulting in a 15% loss for the investor. This mechanism ensures no value is lost for the investment if market losses stay within a certain percentage of the buffer limit.

Cap Rates and Participation Rates

Cap rates and participation rates are key components of buffer annuities. Cap rates limit the potential gains, while participation rates determine the portion of market index gains credited. For instance, a smaller buffer generally results in a higher cap rate, which can lead to greater potential market losses. An 80% participation rate on a 10% index gain would result in an 8% annuity growth.

This trade-off between limited upside potential and loss protection is a hallmark of buffered annuities. Unlike investing in an index fund, buffer annuities do not provide direct ownership of the underlying securities.

Surrender Periods and Charges

Surrender periods and charges are another key aspect of buffer annuities:

Most buffer annuities include a surrender period that can last up to six years.

Penalties for early withdrawals are known as surrender charges.

These surrender charges can vary but generally apply to withdrawals made during the specified surrender period.

Surrender charges and optional features may result in additional cost to the investor. Knowing the surrender periods and potential surrender charges during the specified period helps investors avoid unexpected additional costs.

Comparing Buffer Annuities to Other Annuity Types

Buffer annuities provide a unique blend of features that draw from both fixed indexed annuities and variable annuities, catering to investors’ needs for both growth potential and risk mitigation.

Unlike mutual funds, buffer annuities are insurance products and do not involve direct investment in securities.

This section will compare buffer annuities with other common annuity types to highlight their distinct advantages and limitations.

Buffer Annuities vs. Fixed Indexed Annuities

Buffer annuities allow investors to absorb a certain level of market losses, providing downside protection. In contrast, fixed rate indexed annuities offer a fixed minimum rate, which protects against market losses but typically results in limited gains.

Individuals with greater risk tolerance may prefer buffer annuities for their potential higher returns.

Buffer Annuities vs. Traditional Variable Annuities

Traditional variable annuities expose investors to market volatility without a protective buffer. They offer greater potential for gains but also come with more risk. A variable annuity can provide a different approach to managing these risks.

Buffer annuities, on the other hand, provide a predetermined cushion against losses, making them a safer option for risk-averse investors.

Registered Index Linked Annuities

Registered index linked annuities, developed post-Great Recession, link growth to market index movements, offering a buffer that covers losses up to a specified amount while considering index performance and the particular index. If losses exceed this limit, the investor may lose principal in a registered index linked annuity.

Compared to fixed indexed annuities, registered index linked annuities allow for greater market participation, making them an appealing indexed annuity investment vehicle for those seeking higher returns.

Registered index linked annuities are subject to oversight by the exchange commission, which affects their registration and sales process.

Practical Considerations for Investing in Buffer Annuities

Investing in buffer annuities requires careful consideration of various factors to ensure you can invest directly in options that align with your financial objectives and risk tolerance. Buffer annuities can also be used alongside traditional retirement accounts to diversify your retirement savings strategy.

This section will provide practical advice on evaluating risk tolerance, understanding market conditions, and consulting a financial advisor for advisory services. Keep in mind that while buffer annuities offer tax deferral, you will eventually need to pay taxes on earnings when you withdraw funds.

Evaluating Risk Tolerance

Assessing your risk tolerance is essential when considering buffer annuities. The performance of these annuities is linked to a market index and selected protection level. Knowing your comfort level with downside risk will guide you in determining the appropriate buffer level and investment choices.

Understanding Market Conditions

Market conditions play a significant role in the performance of buffer annuities. During periods of market instability, these annuities can limit losses, allowing you to retain some of your capital.

Being aware of current and future results market conditions is essential for making informed investment decisions.

Consulting a Financial Advisor

Consulting a financial advisor before investing in buffer annuities can provide personalized strategies and emotional support during investment volatility. They can also help you understand the critical aspects of the annuity contract and ensure informed decision-making.

However, financial advisors do not provide legal or tax advice. For specific legal or tax matters, investors should consult appropriately licensed professionals.

Tax Implications of Buffer Annuities

Understanding the tax implications of buffer annuities is crucial for managing your investments effectively. These annuities are subject to tax treatment similar to other types of annuities.

Tax-Deferred Growth

Buffer annuities offer tax deferred growth, allowing you to postpone taxes on your earnings until withdrawal. This tax-deferred growth means your investments can compound without immediate tax liabilities, enhancing your growth potential. A deferred annuity can be a valuable option for those seeking long-term financial strategies.

Ordinary Income Tax on Withdrawals

Withdrawals from buffer annuities are considered ordinary income, which can increase your tax liabilities if you’re in a higher tax bracket. Understanding this tax treatment is crucial for managing your retirement income and financial liabilities during retirement, and consulting a tax professional can provide valuable tax advice.

Use Cases for Buffer Annuities

Buffer annuities are suitable for various investment strategies, offering potential for higher gains while balancing growth with protection against market losses.

Buffer annuities can also be structured to provide regular income payments during retirement, helping retirees plan for steady cash flow.

Retirement Planning

In retirement planning, buffer annuities can help provide secure income while minimizing exposure to market fluctuations. They offer a mechanism for safeguarding capital while allowing for potential growth linked to market performance.

Conservative Investment Strategy

Buffered annuities can serve as a safer investment option for those looking to avoid direct interest rates risks associated with bonds. They provide steady income without high risk, making them suitable for conservative investors. A buffered annuity can also be considered for those seeking similar benefits. Additionally, some buffer annuities offer low fees, making them attractive for conservative investors seeking cost-effective solutions.

Volatile Market Protection

Buffer annuities are designed to provide downside protection while still allowing for market-linked growth. They absorb initial market losses up to a set percentage, creating a safety net for investors during volatile market conditions.

Summary

Buffer annuities offer a unique blend of growth potential and downside protection, making them an attractive investment option in today’s volatile market. By understanding their key features, comparing them to other annuity types, and considering practical investment advice, you can determine if buffer annuities align with your financial goals.

It is important to remember that all guarantees and downside protections provided by buffer annuities are subject to the claims paying ability of the issuing insurance company.

Whether you’re planning for retirement or seeking a conservative investment strategy, buffer annuities provide a compelling option to balance risk and reward. Consider consulting a financial advisor to explore how buffer annuities can fit into your overall investment plan.

Frequently Asked Questions

What are buffer annuities?

Buffer annuities are financial instruments that offer market downturn protection while still allowing for potential growth tied to market performance. They serve as a balanced option for investors seeking security alongside the opportunity for investment gains.

How do buffer annuities work?

Buffer annuities provide downside protection by linking investment growth to a market index, absorbing a portion of market losses while offering potential benefits based on index performance. This design allows for balanced risk and reward during the investment term.

What is the buffer mechanism in buffer annuities?

The buffer mechanism in buffer annuities serves to absorb initial market losses of 10% to 30%, thereby protecting investors while still providing opportunities for growth. This feature enhances investment security, making buffer annuities appealing for risk-averse individuals.

How are withdrawals from buffer annuities taxed?

Withdrawals from buffer annuities are taxed as ordinary income, potentially elevating tax liabilities for those in higher tax brackets. It is essential to consider this impact when planning withdrawals.

What are the key differences between buffer annuities and traditional variable annuities?

The key difference between buffer annuities and traditional variable annuities lies in risk management; buffer annuities offer a protective cushion against market losses, whereas traditional variable annuities do not provide this safeguard and expose investors fully to market fluctuations.